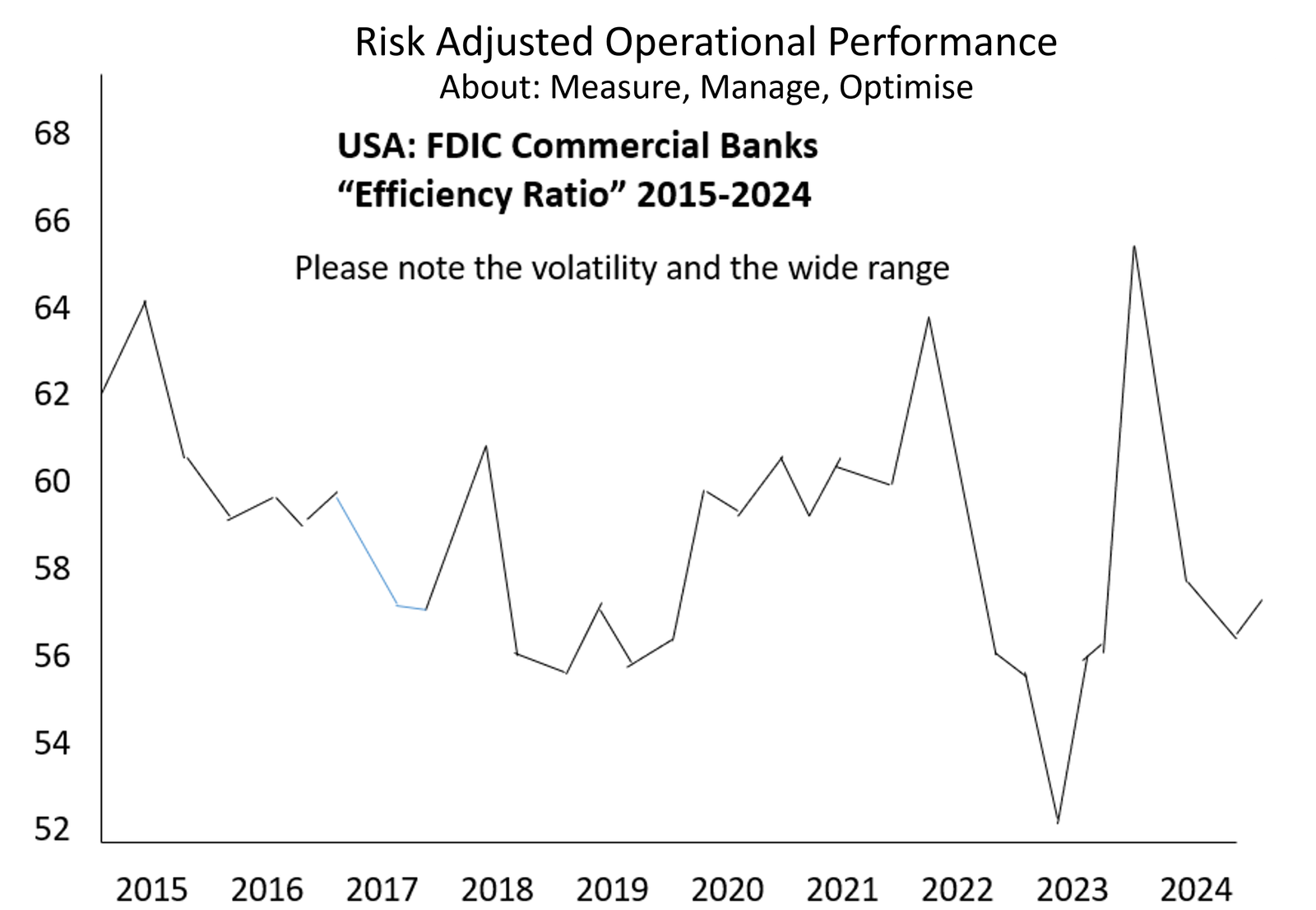

- The calculation of the cost to income ratio is non-standard. Some banks make adjustments for loan provisions and write offs. Further, the ratio is not risk-adjusted.

The American Banker in an article tilted, A Fickle Measure: Efficiency Ratios Resume Slide, in 2012, opined “efficiency can be a slippery concept.

https://www.americanbanker.com/news/a-fickle-measure-efficiency-ratios-resume-slide

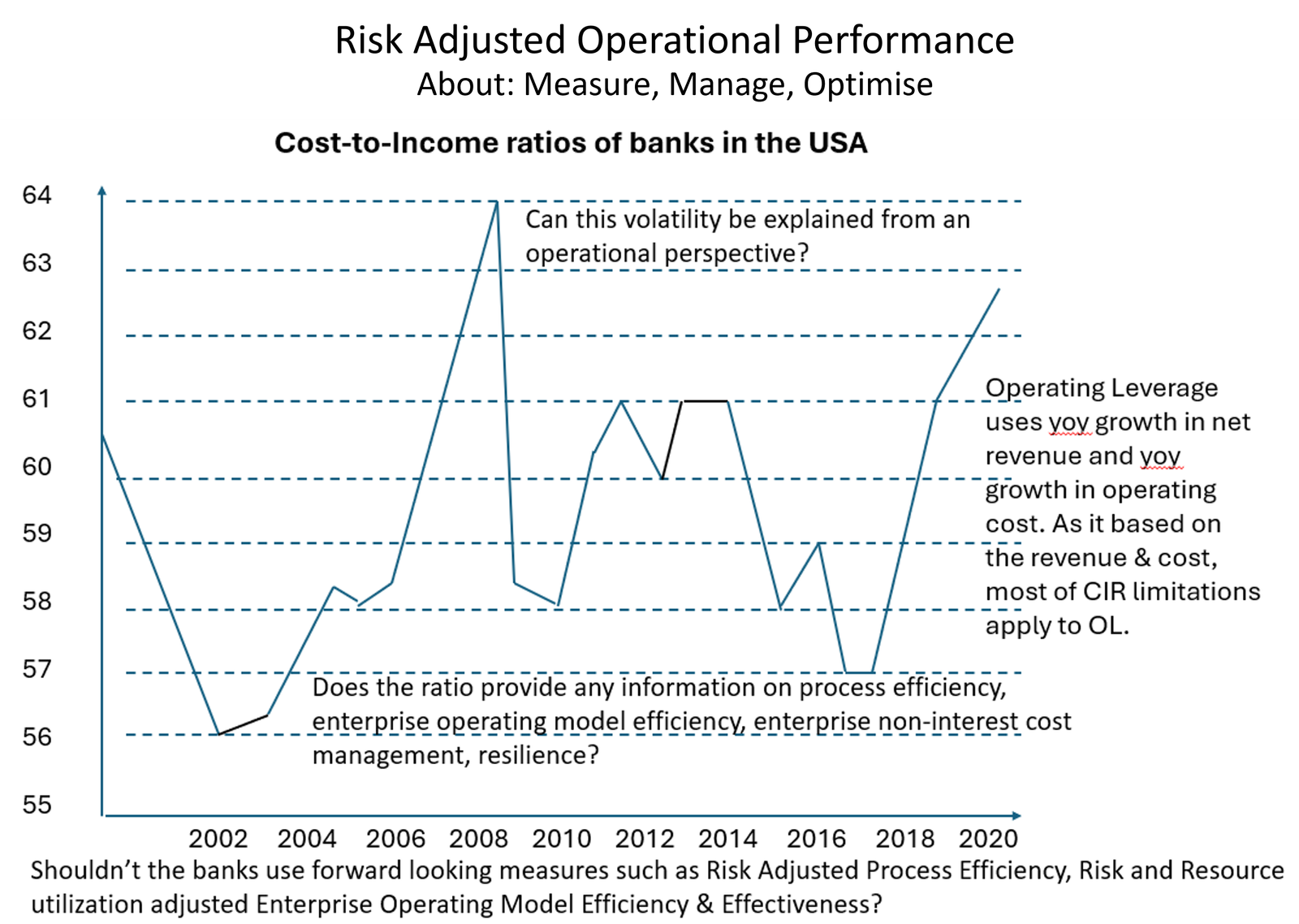

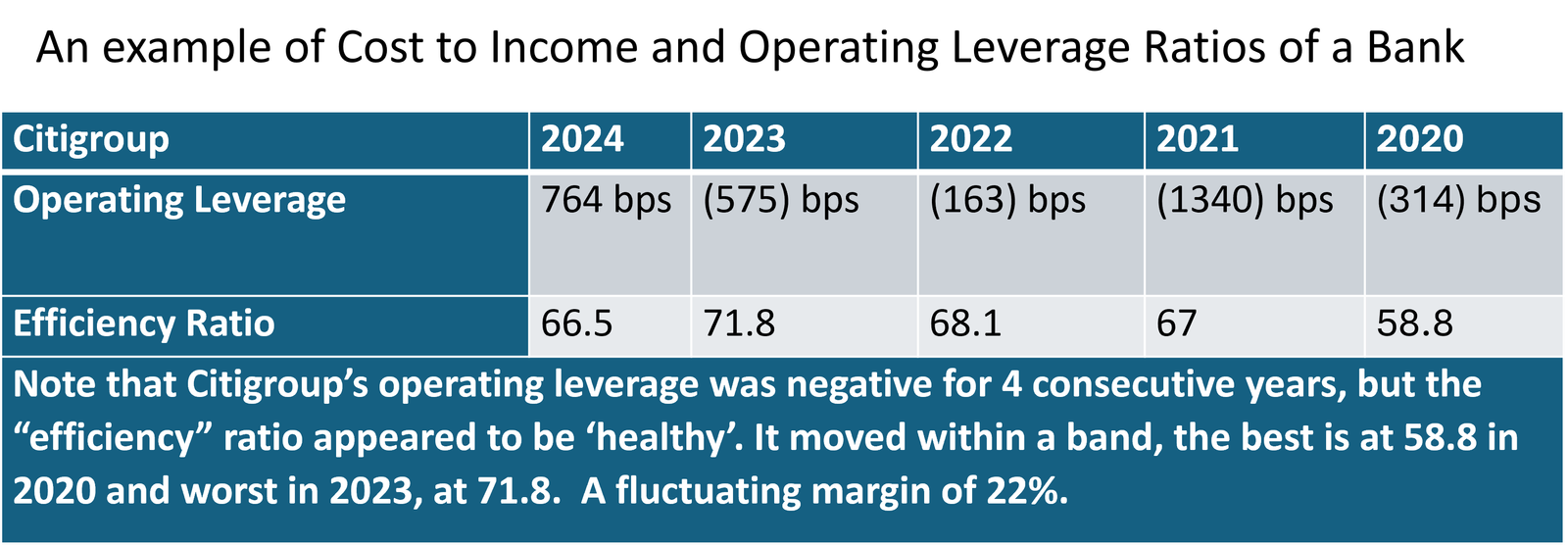

- There are a small number of banks who report operating leverage. The underlying calculation uses the same financial variables (book keeping data items) that go into the cost to income ratio. Operating leverage is calculated as the year-over-year percentage change of growth in revenue vis-à-vis Growth in operating cost

- It suffers from the same limitations as the cost-to-income ratio as the input data category is the same for both ratios.

- A 2006 article in the American Banker titled ‘What Is Operating Leverage, Exactly?’ acknowledges that the term lacks a common definition.https://www.americanbanker.com/news/what-is-operating-leverage-exactly

The imperative need for improving resilience & measuring risk adjusted efficiency & effectiveness

Five sample references that establish the need for risk adjusted operational performance measures are provided below:

Many banks have shortcomings related to cost allocation https://www.bankingsupervision.europa.eu/press/supervisory-newsletters/newsletter/2023/html/ssm.nl230215.en.html

Nine of the top banks and building societies operating in the UK accumulated at least 803 hours, the equivalent of more than 33 days, of unplanned technology and systems outages in the last two years https://committees.parliament.uk/committee/158/treasury-committee/news/205611/more-than-one-months-worth-of-it-failures-at-major-banks-and-building-societies-in-the-last-two-years/#:~:text=Nine%20of%20the%20top%20banks%20and%20building%20societies,new%20data%20published%20by%20the%20Treasury%20Committee%20shows

Four pillars are critical to maintaining trust: capital to absorb losses, liquidity to mitigate and withstand runs, operational resilience to maintain critical operations, and recovery planning to ensure options in stress https://www.occ.gov/news-issuances/speeches/2024/pub-speech-2024-79.pdf

Focusses on an event & process based enterprise operating model. It encourages banks to transform their siloed operating modelhttps://www.fsa.go.jp/news/r4/ginkou/20230427/04.pdf

U.S. Subcommittee on Financial Institutions of the House Committee on Financial Services, Ms Margaret E.Tahyar

Risk Adjusted Operational Performance Measurement is a smart reform. https://www.congress.gov/119/meeting/house/118144/witnesses/HHRG-119-BA20-Wstate-TahyarM-20250429.pdf